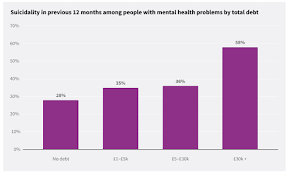

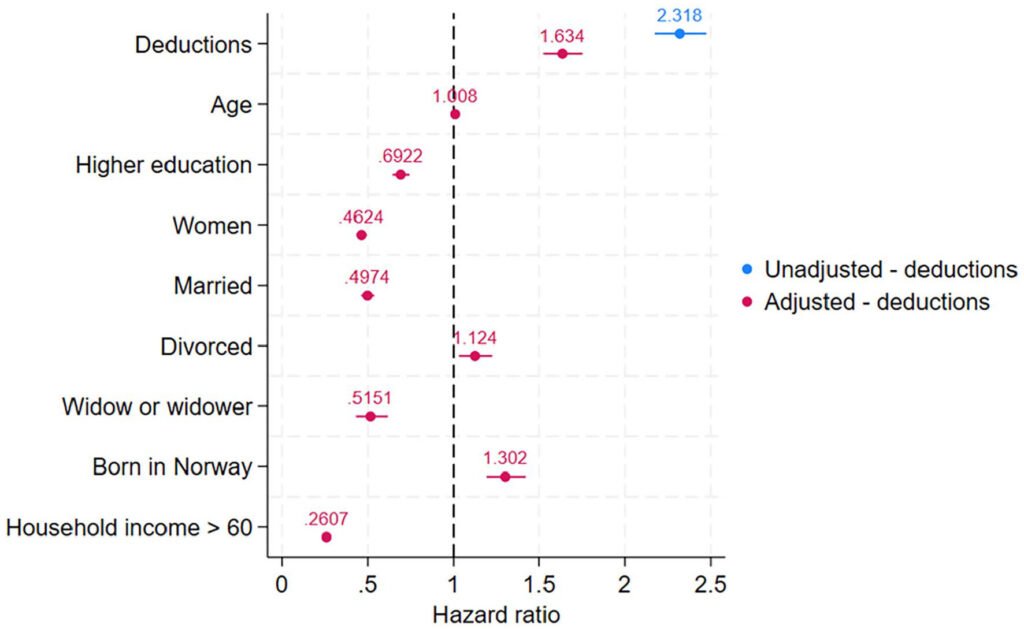

Financial stress is one of the most significant pressures many people face in life. When debts pile up—credit card balances, personal loans, mortgages, or medical bills—the emotional and psychological burden can become overwhelming. Unfortunately, research has shown a disturbing link between heavy debt and increased risk of suicide.

This article explores the connection between financial distress and mental health, the warning signs, and practical solutions to manage debts and prevent crises. It’s designed to raise awareness, provide guidance, and promote proactive financial and emotional health strategies.

1. Understanding the Debt-Suicide Connection

a. Why Debt Causes Extreme Stress

Debt impacts more than just finances; it affects emotional well-being:

- Chronic stress: Persistent worry over unpaid bills and mounting interest can affect mental health.

- Sleep disruption: Anxiety about money can lead to insomnia or poor-quality sleep.

- Relationship strain: Financial stress often causes tension among family members or partners.

- Loss of self-esteem: Feeling trapped in debt can erode confidence and self-worth.

b. Research Insights

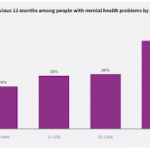

Multiple studies have confirmed a link between heavy financial debt and suicidal behavior:

- Individuals with unmanageable debt are more likely to experience depression and anxiety.

- Bankruptcy or foreclosure increases psychological strain, sometimes triggering extreme outcomes.

- Young adults with student loan debt report higher levels of stress and suicidal ideation.

Financial distress isn’t the sole cause of suicide but acts as a significant risk factor when combined with mental health challenges.

2. Types of Debt That Contribute to Financial Stress

While any debt can cause stress, certain types are more strongly associated with psychological distress:

a. Credit Card Debt

- High interest rates make repayment challenging.

- Minimum payments often prolong indebtedness, increasing stress.

b. Medical Debt

- Unexpected medical bills can spiral out of control, even with insurance.

- Medical debt is a leading cause of bankruptcy in many countries.

c. Personal Loans and Payday Loans

- Short-term loans with high-interest rates can create a cycle of debt.

- Borrowers may struggle to repay while facing interest compounding.

d. Mortgages and Foreclosures

- Missing mortgage payments increases the risk of foreclosure.

- Homeowners may feel trapped, fearing loss of shelter and security.

e. Student Loans

- Young adults often face decades of repayment.

- Limited income and rising living costs compound stress.

3. Warning Signs of Debt-Induced Stress

Recognizing early warning signs can help prevent extreme outcomes. Common indicators include:

- Emotional symptoms: Anxiety, depression, irritability, or hopelessness.

- Behavioral changes: Avoiding bills, withdrawing socially, or increased substance use.

- Physical symptoms: Headaches, high blood pressure, or insomnia.

- Financial avoidance: Ignoring collection calls or hiding financial information from family.

Early recognition and intervention are critical. Friends, family, and professionals can make a lifesaving difference.

4. Strategies to Manage Debt and Reduce Stress

a. Create a Comprehensive Budget

- Track all income and expenses.

- Identify areas to reduce spending.

- Prioritize essential payments (housing, utilities, food).

b. Debt Consolidation

- Combine multiple debts into a single loan with lower interest.

- Reduces monthly payment complexity and may lower interest costs.

c. Negotiate with Creditors

- Many lenders are willing to negotiate reduced interest rates, payment plans, or settlements.

- Proactive communication can relieve immediate stress.

d. Seek Professional Financial Counseling

- Certified credit counselors can provide structured repayment plans.

- Guidance helps restore control and reduces anxiety.

e. Government and Community Assistance Programs

- Some programs provide emergency funds, debt relief, or low-interest loans.

- Social services may help cover basic needs to ease financial pressure.

5. Emotional and Mental Health Support

Financial stress often intertwines with mental health challenges. Addressing both is essential:

a. Therapy and Counseling

- Cognitive-behavioral therapy (CBT) is effective for anxiety and depression related to financial stress.

- Mental health professionals can provide coping strategies and emotional support.

b. Support Groups

- Debt support groups offer shared experiences and practical advice.

- Peer support reduces isolation and stigma.

c. Crisis Resources

- Hotlines and emergency services exist for individuals experiencing suicidal thoughts.

- Examples: 988 in the U.S., Samaritans in the U.K., or local crisis lines worldwide.

d. Stress Reduction Techniques

- Meditation, mindfulness, and physical activity improve resilience.

- Healthy routines reinforce emotional stability while tackling debt.

6. Real-Life Case Studies

Case Study 1: Credit Card Overload

John, a 35-year-old professional, accumulated $50,000 in credit card debt due to overspending and emergency expenses. Anxiety and insomnia escalated to panic attacks. After seeking financial counseling and negotiating a consolidation loan, John regained control, avoiding further mental health decline.

Case Study 2: Medical Debt Crisis

Maria faced $100,000 in medical bills following an unexpected illness. She reported depression and hopelessness. By enrolling in hospital payment assistance programs, seeking therapy, and creating a structured repayment plan, she stabilized her finances and mental health.

These examples highlight the importance of combining financial planning with emotional support.

7. Preventative Measures for Financial Well-Being

a. Build an Emergency Fund

- Savings covering 3–6 months of living expenses can prevent reliance on high-interest loans.

b. Live Within Means

- Avoid lifestyle inflation even as income grows.

- Track spending to prevent accumulating unnecessary debt.

c. Educate Yourself on Financial Literacy

- Understand interest rates, compounding, and budgeting.

- Knowledge empowers better decision-making and reduces stress.

d. Avoid Predatory Loans

- Be cautious of payday loans, high-interest personal loans, or deceptive financing.

8. Warning Signs That Professional Help is Needed

- Persistent thoughts of hopelessness or self-harm.

- Chronic inability to meet financial obligations.

- Withdrawal from family, friends, or daily responsibilities.

- Dependence on substances to cope with stress.

Seeking help early can save both life and financial stability.

9. Government and NGO Programs for Debt Relief

- Bankruptcy options: Chapter 7 or 13 (U.S.) can provide structured relief.

- Debt management plans: Approved by credit counselors to reduce interest and consolidate payments.

- Emergency aid programs: Food assistance, rental relief, and utility support.

- Mental health programs: Many include financial counseling and suicide prevention resources.

Utilizing these programs can reduce financial pressure and improve emotional well-being.

10. The Role of Employers and Communities

Workplaces and communities can play a critical role:

- Employee assistance programs (EAPs) provide confidential financial and mental health counseling.

- Community workshops can improve financial literacy.

- Peer support initiatives reduce isolation and encourage early intervention.

11. Key Takeaways

- Heavy debt is a significant risk factor for emotional distress and suicidal behavior.

- Early recognition of stress and warning signs is critical.

- Professional financial and mental health support can save lives.

- Strategic debt management, budgeting, and assistance programs reduce risk.

- Prevention requires education, planning, and building financial resilience.

12. Conclusion: Addressing Debt Before It Becomes Overwhelming

Debt is more than a financial challenge—it can be a severe emotional and mental health risk. Awareness, proactive management, and seeking support are essential steps in preventing financial stress from escalating to a crisis.

While heavy debts can feel insurmountable, solutions exist:

- Create structured repayment plans

- Seek counseling and therapy

- Leverage government and community programs

- Build financial literacy and emergency savings

Recognizing the emotional weight of debt and acting early empowers individuals to regain control over their finances and mental health. Financial problems should never be faced alone—resources, support, and strategic planning are key to overcoming heavy debts and preventing tragic outcomes.

Summary:

The Royal Bank of Scotland (RBS) will be investigated following suggestions that irresponsible lending by them was the cause of the suicide of one of its customers.

Richard Cullen, 65, took his own life in January 2005 after amassing credit card debts of �130,000 – �35,000 of which was owed to the RBS group.

Banking watchdog, the Banking Code Standards Board (BCSB), will now investigate RBS’s lending practices amid concerns that it failed to put two and two together and…

Keywords:

tml, loan, loans, debt consolidation, credit cards

Article Body:

The Royal Bank of Scotland (RBS) will be investigated following suggestions that irresponsible lending by them was the cause of the suicide of one of its customers.

Richard Cullen, 65, took his own life in January 2005 after amassing credit card debts of �130,000 – �35,000 of which was owed to the RBS group.

Banking watchdog, the Banking Code Standards Board (BCSB), will now investigate RBS’s lending practices amid concerns that it failed to put two and two together and appreciate the extent of Mr Cullen’s debt problems.

I find it extraordinary that this has happened, chief executive Seymour Fortescue told BBC’s Panorama, I think it is a case of the right hand not knowing what the left hand is doing and there is no excuse for that. This is wrong.

In November 2004, the limit on Mr Cullen’s Tesco Personal Finance card, (a card which is operated by RBS), was increased by �1,000 to �7,700, despite the fact that two weeks earlier RBS had been chasing him for arrears owed on his Mint credit card.

In total the mechanic owed RBS more than double his annual salary. Spread over four cards, the RBS debt cost him more than �4,200 in interest and charges in the 12 months running up to his death.

Mr Fortescue confirmed that the BCSC is seeking the authority of the Cullen family to conduct a probe into the practices of the bank.

Meanwhile, the bank has defended itself against charges of irresponsible lending.

In a statement issued to Panorama The Royal Bank of Scotland said: Mr Cullen did not make us aware of the extent of the debt of approximately �100,000, he subsequently incurred with 16 other providers. We have a rigorous and responsible process for managing customer debt.

Mr Cullen also owed money on a further 18 credit cards held with different providers.

� Adfero Ltd

Tinggalkan Balasan