Personal loans can be an effective financial tool when used responsibly. Whether you want to consolidate debt, cover unexpected expenses, or finance a large purchase, personal loans provide flexibility and access to funds. However, they also carry risks, including high interest rates, fees, and potential impact on your credit score. Understanding how personal loans work and how to use them wisely is essential to maximize benefits while minimizing risks.

This article provides practical hints, expert tips, and strategies for using personal loans effectively.

1. What Is a Personal Loan?

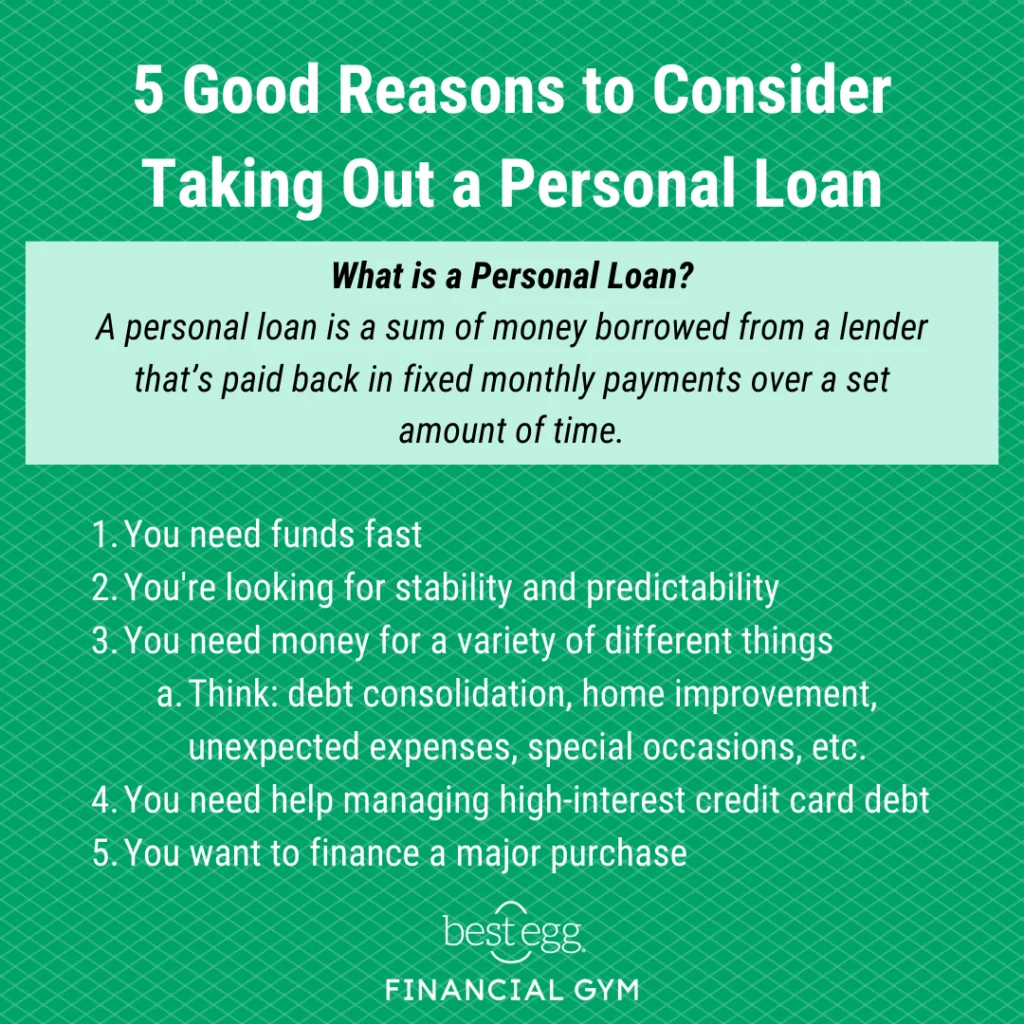

A personal loan is a borrowed sum of money that you repay in fixed installments over a set period, typically ranging from one to seven years. Unlike credit cards, personal loans provide a lump sum upfront with a fixed interest rate and repayment schedule.

Key Features:

- Fixed or variable interest rates: Most personal loans have fixed rates, making payments predictable.

- Fixed repayment schedule: Payments are generally monthly.

- Unsecured or secured: Some loans require collateral, while most personal loans are unsecured.

- Loan amount flexibility: Personal loans range from a few hundred to tens of thousands of dollars.

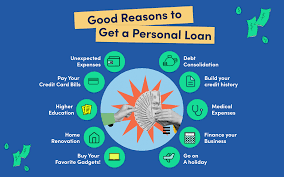

2. Common Uses for Personal Loans

Personal loans can serve various purposes:

a. Debt Consolidation

- Combine multiple debts (credit cards, medical bills, small loans) into one payment.

- Can reduce interest rates and simplify finances.

b. Major Purchases

- Financing furniture, electronics, or home improvement projects.

- Often cheaper than using high-interest credit cards.

c. Emergency Expenses

- Cover medical bills, car repairs, or sudden household expenses.

- Provides quick access to cash without dipping into savings.

d. Special Occasions

- Weddings, vacations, or family events can be funded responsibly with a personal loan.

3. Types of Personal Loans

Understanding the different types can help you choose the right loan:

a. Unsecured Personal Loans

- No collateral required.

- Higher interest rates due to increased risk to the lender.

b. Secured Personal Loans

- Backed by assets such as a car, home, or savings account.

- Lower interest rates but risk of losing collateral if you default.

c. Fixed-Rate Loans

- Interest rate remains constant throughout the loan term.

- Easier to budget monthly payments.

d. Variable-Rate Loans

- Interest rates fluctuate with market conditions.

- Can be lower initially but may increase over time.

e. Payday and Short-Term Loans (Use with caution)

- Very short repayment periods and extremely high interest rates.

- Often considered last-resort options due to predatory lending risks.

4. Factors to Consider Before Taking a Personal Loan

Before borrowing, evaluate the following:

a. Interest Rates

- Compare multiple lenders.

- Understand whether rates are fixed or variable.

b. Loan Terms

- Consider repayment length: shorter terms have higher payments but lower total interest.

- Longer terms reduce monthly payments but increase total cost.

c. Fees and Penalties

- Origination fees, late payment penalties, and prepayment penalties can affect affordability.

d. Your Credit Score

- Better credit usually results in lower interest rates.

- Check your credit report for errors before applying.

e. Income and Debt-to-Income Ratio

- Lenders will evaluate your ability to repay.

- A high debt-to-income ratio may reduce approval chances or increase rates.

5. Tips for Managing Personal Loan Applications

a. Shop Around

- Compare interest rates, fees, and terms from banks, credit unions, and online lenders.

b. Prequalification

- Many lenders offer prequalification with a soft credit check, which does not affect your credit score.

c. Borrow Only What You Need

- Avoid overborrowing; it increases debt burden unnecessarily.

d. Read the Fine Print

- Understand all fees, penalties, and conditions before signing.

e. Avoid Multiple Applications at Once

- Multiple hard inquiries can negatively affect your credit score.

6. Strategies for Using Personal Loans Wisely

a. Debt Consolidation Plan

- Use the loan to pay off higher-interest debts first.

- Keep old accounts open to maintain credit history but avoid accumulating new debt.

b. Emergency Fund Backup

- Consider personal loans for emergencies if you have no savings, but plan repayment carefully.

c. Budgeting

- Include loan payments in your monthly budget to avoid missed payments.

d. Automated Payments

- Set up automatic payments to ensure timely repayment and avoid penalties.

e. Pay Extra When Possible

- Reduces total interest paid and shortens the loan term.

7. Pitfalls to Avoid with Personal Loans

- Using loans for non-essential spending – Avoid financing vacations or luxury items unless affordable.

- Missing payments – Late payments can hurt your credit score and trigger fees.

- Ignoring interest costs – Long terms can make loans expensive if interest accumulates.

- Overextending credit – Borrowing too much can lead to financial stress.

- Falling for predatory lenders – Avoid payday or high-fee lenders without clear terms.

8. Case Studies

Case Study 1: Debt Consolidation Success

Sarah had $20,000 in credit card debt at 18–22% interest rates. She secured a $20,000 personal loan at 9% and consolidated her debts. Her monthly payments decreased, interest costs were reduced, and she became debt-free in three years.

Case Study 2: Emergency Medical Expenses

James faced unexpected surgery costs of $12,000. Using a personal loan, he paid the hospital quickly, avoided high-interest credit card debt, and repaid the loan over two years, protecting his credit and savings.

These examples show how strategic borrowing can provide relief and financial control.

9. Alternatives to Personal Loans

Before taking a personal loan, consider alternatives:

- Credit Card 0% APR Offers – Short-term interest-free financing for smaller amounts.

- Home Equity Loans or Lines of Credit – Lower rates but secured by your property.

- Peer-to-Peer Lending – Often offers competitive rates.

- Employer Assistance Programs – Some provide interest-free or low-interest loans for emergencies.

10. Building a Healthy Borrowing Habit

a. Understand Your Finances

- Track income, expenses, and savings.

- Know how much you can realistically repay.

b. Avoid Impulse Borrowing

- Loans should meet real financial needs, not momentary wants.

c. Use Loans to Build Credit

- Timely repayment improves credit score, opening doors to lower-cost financing in the future.

d. Review Loan Performance

- Monitor balances, interest accumulation, and payment schedules regularly.

11. Key Takeaways

- Personal loans are flexible, but they must be used responsibly.

- Always compare lenders, terms, and interest rates.

- Use loans for debt consolidation, emergencies, or essential purchases.

- Maintain a budget, automated payments, and a clear repayment plan.

- Avoid predatory lenders and high-risk loan types.

12. Conclusion: Borrow Smart, Borrow Wisely

Personal loans can be a valuable tool when used strategically. By understanding how they work, managing repayments carefully, and avoiding common pitfalls, borrowers can reduce financial stress, consolidate debts, or cover necessary expenses effectively.

The key to personal loan success lies in planning, research, and disciplined repayment. Smart borrowing builds financial stability, improves creditworthiness, and can be a stepping stone toward achieving larger financial goals.

When used responsibly, personal loans are more than just a source of funds—they’re a tool for financial empowerment.

Summary:

Are you thinking of taking out a personal loan! If the answer is yes then you have to ask yourself some questions first. This will make sure that the loan you choose is the right one to suit your needs.

Keywords:

Loan, APR, interest, rate, repayments, credit, lender, penalties, borrow, rating

Article Body:

Are you thinking of taking out a personal loan! If the answer is yes then you have to ask yourself some questions first. This will make sure that the loan you choose is the right one to suit your needs.

Below are some of the most common questions you should be asking.

Do I really need a personal loan?

You have to ask yourself if the purchase you are about to buy is necessarily, as you may have this debt for a year or two.

Can I afford to takeout a personal loan?

This is properly the most important question you will have to ask yourself, debt advisers says that a non- mortgage monthly repayment debt should not be anymore than 5% of your net income. This is the total you walkout with after tax, say you take home �2000 a month then the most you should be paying back is about a �100 a month.

How much should I borrow?

Most lenders offer a cheaper APR on a larger loan; each lender has their different levels of interest rates and will change them with accordance to how much you borrow. Sometimes it�s best to up your loan just a small bit to get the best interest rate.

For example maybe you only want a loan of �4.500 your APR maybe 10.5% but if you go for a �5,000 loan the APR drops to 9.6%. So over all you may end up saving by taking out a bit more just something to watch out for.

Where do I go for a personal loan?

Most people think of the bank first nothing wrong with that, but know there are so many places to look. Everywhere you turn you see adverts for loans including the newspapers, TV, mail, supermarkets and the Internet. The competition at the moment from the lenders is great; they all want your business so there are some great deals on offer. You just have to look for them take your time and you are sure to get the best deal around

Will I be covered if I become ill or unemployed?

Most lenders will have PPI (payment protection Insurance) please check the policy carefully and ask questions. As not all these policies will cover you and they can be expensive, sometime it�s best to shop around for a different policy.

Can I pay my loan off early?

Yes you can and unbelievably 60% of people do, again check with your lender as some add on penalties for paying off your loan early. Some lenders charge two or three months interest unbelievable but true.

What happens if I get turned down for a loan?

First check why is it because your credit rating is poor or is it because you�re asking for too much money. If your income is low you may be asking for too much, if this is the case reduce your request. If it�s poor credit rating check out why and try and sort that out first, before you reapply

Hopefully these answers will help you, just remember workout what you need the loan for first, then make sure you can afford to make the repayments. Take your time when looking for your personal loan, as there are some great deals out there at the moment.

Tinggalkan Balasan